Games can be categorised along a continuum based on their reliance on luck or skill. Roulette, for instance, is purely a game of chance. Despite occasional wins, the player will lose in the long run due to the wheel’s inherent design and the odds a player must accept. Conversely, chess is a game of skill, where a novice stands little chance against a grandmaster. While investing leans more towards the skill end of the spectrum, macroeconomic factors, geopolitical events and other unforeseen incidents introduce an element of luck into the equation, particularly over the short term.

Put differently, luck can be good or bad and can present as a favourable or unfavourable hand of cards. However, luck is an external, unstable factor that we cannot control or replicate. To counter this, we need to focus on what we can control: the skilful application of a strong investment philosophy and process that has proven to work through various market cycles. This is a far more reliable determinant of success than luck over the long term. Joshua Singer, business analyst and Jithen Pillay, portfolio manager, discuss, looking at the current environment.

2024 is a year of heightened uncertainty, with the hands we have been dealt requiring careful consideration. From the potential for adverse election outcomes impacting global stability to the looming threat of stubborn inflation, and the continued economic challenges in South Africa, the landscape is complex. However, amidst these challenges, there are also potential upsides, such as the improving sentiment in Namibia. Navigating these factors will be crucial for managing risk and preserving capital while positioning ourselves to capitalise on emerging opportunities.

The first hand we have been dealt is the potential of adverse election outcomes, with half of the world’s population voting in 2024, as seen in Figure 1. Normally, when thinking about investments, we do not pay special attention to politics – but this is not a normal election cycle; wide policy disparity has the potential to materially affect some of our underlying holdings. The various elections are taking place against the backdrop of a world increasingly divided along both geopolitical and social lines. In our view, 2024 has above-average political risk. We have already witnessed a major decline in support for the ruling African National Congress (ANC) in neighbouring South Africa (SA), which has led to the formation of a Government of National Unity (GNU). While this shift towards coalition politics can be seen as a sign of a maturing democracy, it also brings with it an element of unpredictability.

The next hand is the possibility of higher inflation and interest rates – especially in developed markets. Even though we are based in Southern Africa and make investment decisions based on company fundamentals, macroeconomic factors in developed markets impact our investment environment. Drawing on the findings from Allianz Research and our offshore partner, Orbis, we need to be cognisant of the “five Ds” driving global inflation:

- Demographics: An ageing workforce and low unemployment are putting upward pressure on wages.

- Decarbonisation: The energy grid needs to transition to renewable energy; however, this requires significant capital investment.

- Deglobalisation: Supply chains are fragmenting as countries move away from using the most economical sources of production, to rather prioritise security of supply from domestic partners or economic allies.

- Debt: Heavily indebted individuals, businesses, and governments are generally more willing to tolerate high inflation as it reduces the real value of the debt. However, this could encourage them to take on more debt, further fuelling inflation.

- Defence spending: To maintain healthy democracies, countries realise they need to spend more on defence compared to recent history.

The third hand is a continued weak South African economy. Many South African companies appear cheap on a headline level. However, this comes with a health warning: The real earnings of these companies, on average, have struggled to grow over the last decade owing to sluggish revenue growth and rising costs (the latter particularly impacted by inefficiencies linked to loadshedding). This impacts us locally not only because SA is part of our investment universe, but also given the close economic ties and interdependencies.

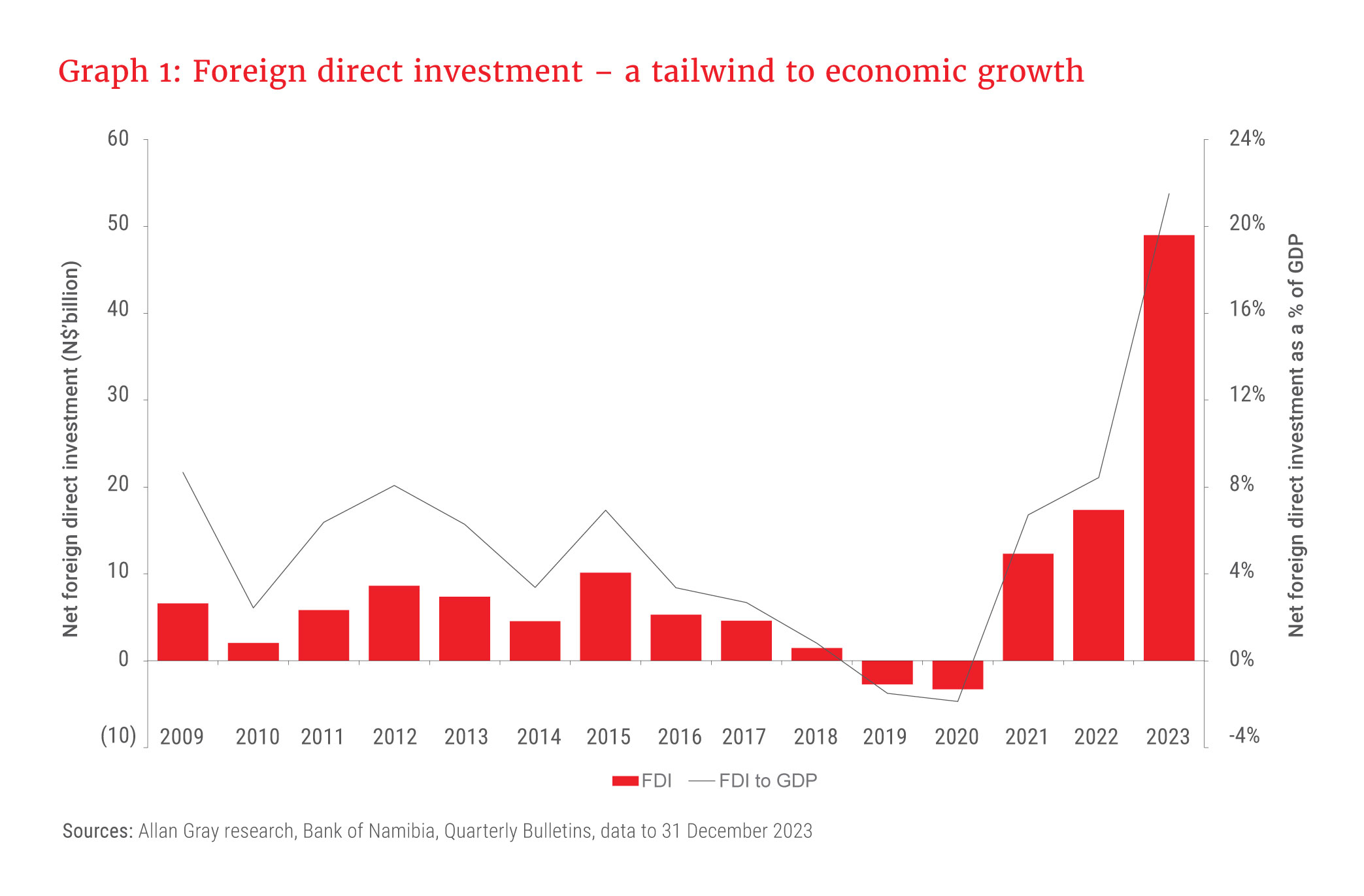

The fourth hand is a positive one – the improving sentiment in Namibia. Foreign direct investment (FDI) into Namibia is at record highs, as shown in Graph 1. This progress is driven by exploration activity in mining, oil and gas, as well as green hydrogen investments. Since Shell’s significant oil discovery in February 2022, several promising well discoveries have positioned Namibia as a potential future hydrocarbon province. If the oil finds prove commercially viable, the impact on our country could be extensive over the long term. We estimate that the taxes and royalties the Namibian government could earn per annum will dwarf the current fiscal deficit, boosting the domestic economy.

Positioned for a wide range of outcomes

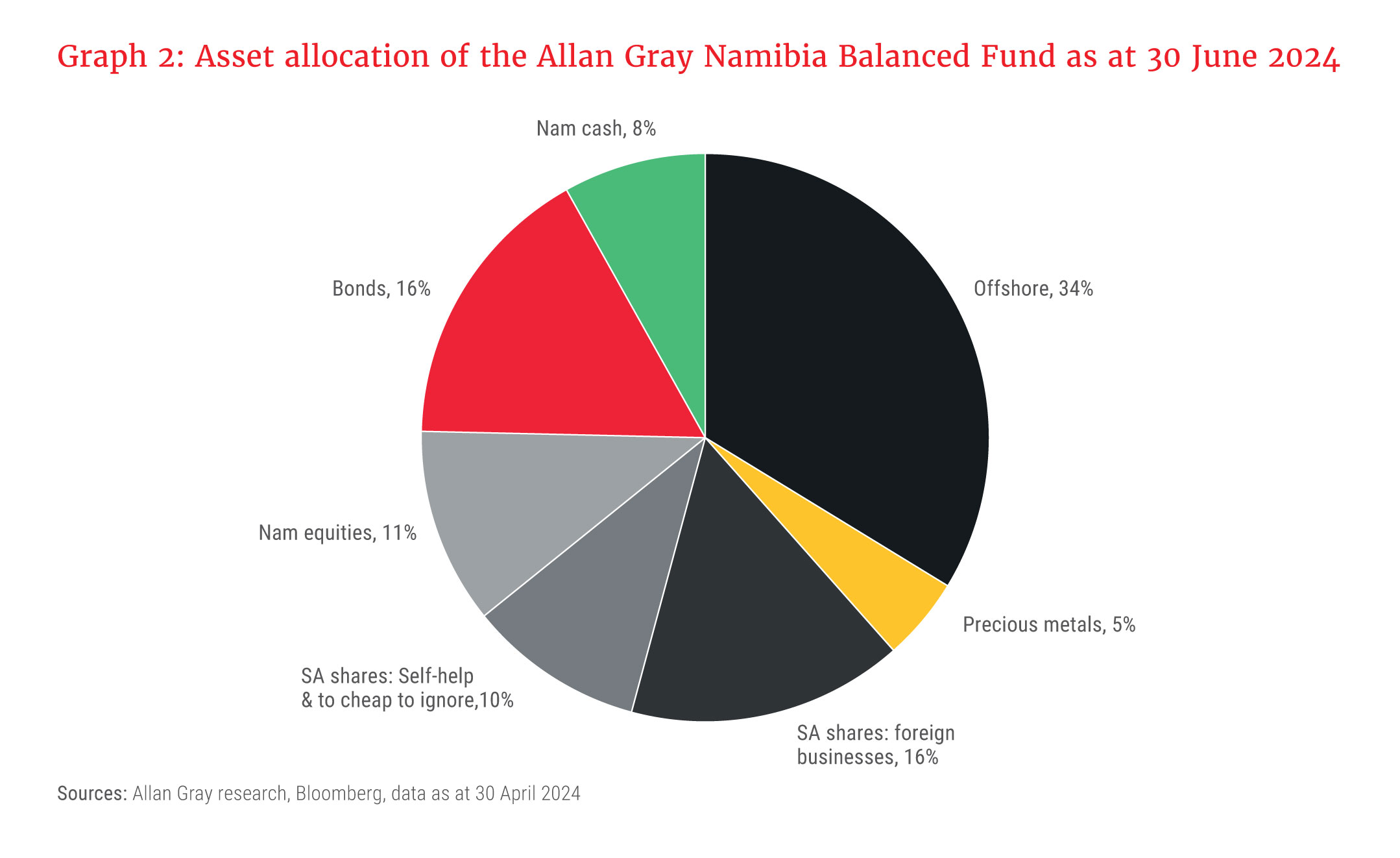

Given the heightened uncertainty and the hands that we have been dealt, which have the potential to deliver binary outcomes, we believe 2024 is a year to minimise risk and preserve capital. We have positioned our portfolios defensively for a wide range of potential outcomes – as shown in Graph 2, which uses the Allan Gray Namibia Balanced Fund’s positioning as an example.

About a third of the portfolio is invested directly offshore, managed by Orbis. Another 16% of the portfolio is invested in shares that happen to be listed in SA but generate most of their earnings offshore, such as British American Tobacco and brewer AB InBev. We favour precious metals and select precious metal miners, as we believe they behave differently from the rest of the market in times of crisis.

The companies we hold that are exposed to the South African economy are built on investment cases that do not rely solely on a reversal of the economic fortunes. We favour SA “self-help” companies, which we believe have internal levers to pull to improve their economics, even if the local economy is weaker than we would have hoped. Examples include Woolworths, Standard Bank and Remgro. Additionally, there are a few SA companies we believe are too cheap to ignore, where things only need to go slightly better for investors to realise decent returns. However, selectivity is crucial, as not all companies in this category are likely to emerge as winners.

Namibian equities have had a stellar run, returning over 20% per annum over the past three years. Despite the recent surge in stock prices, the NSX Local Index has barely outperformed the FTSE/JSE All Share Index over a five-year period. We believe that these businesses are well positioned to benefit should the bullish outlook for the Namibian economy materialise. If not, we believe their attractive starting valuations should limit downside risk.

Perhaps the most evident indicator of rising optimism towards the Namibian economy is Namibian government bonds. For the first time in history, Namibian government bonds trade at lower yields relative to South African government bonds, indicating that investors believe Namibia has a better risk-adjusted return profile versus SA. Despite the rally, we believe the long end of the yield curve is still attractive and we are positioned accordingly. Additionally, we have a significant position in cash, which offers satisfactory real yields and provides optionality should buying opportunities arise.

We believe our positioning should protect client capital across various outcomes, as well as provide the opportunity to earn returns from a range of asset classes as different scenarios unfold.

As the year progresses, the cards will undoubtably be shuffled. Regardless, we will continue to lean on the factors we can control – including the skilful application of our decades-old investment philosophy and process – which guides how we will respond, regardless of circumstance.